Competitive market access and diverse asset segmentation frequently turn localized solar fleets into international investment hubs. The structural conclusions detailed in this feature are lifted straight from our annual 'Top 50 Operational Solar Portfolios Europe 2026' report, compiled by research analyst Zsolt Szalay. This analysis profiles the corporate profiles shaping the Italian utility-scale marketplace.

Key takeaways

- Italy is Europe's third-largest solar asset market, with a cumulative capacity of 43.5 GW.

- Ranked top 50 organizations operate 5.7 GW of assets locally across 26 active companies.

- Domestic entities control only 43.1% of the localized ranked large-scale solar footprint.

Italy's cumulative installed solar capacity reached approximately 43.5 GW at the end of 2025, making it Europe's third-largest solar market. Unlike more uniform landscapes, Italy's solar sector remains evenly distributed across residential systems (27%), Commercial and Industrial (C&I) installations (43%), and large-scale utility projects (30%), which account for 13 GW. Within our top 50 ranking, Italy hosts 5.7 GW of operational solar capacity distributed across 26 companies. This notable number of active portfolio owners makes Italy one of the most competitive and internationally accessible utility-scale ownership markets within the database, with the top 50 accounting for 44% of the local large-scale base.

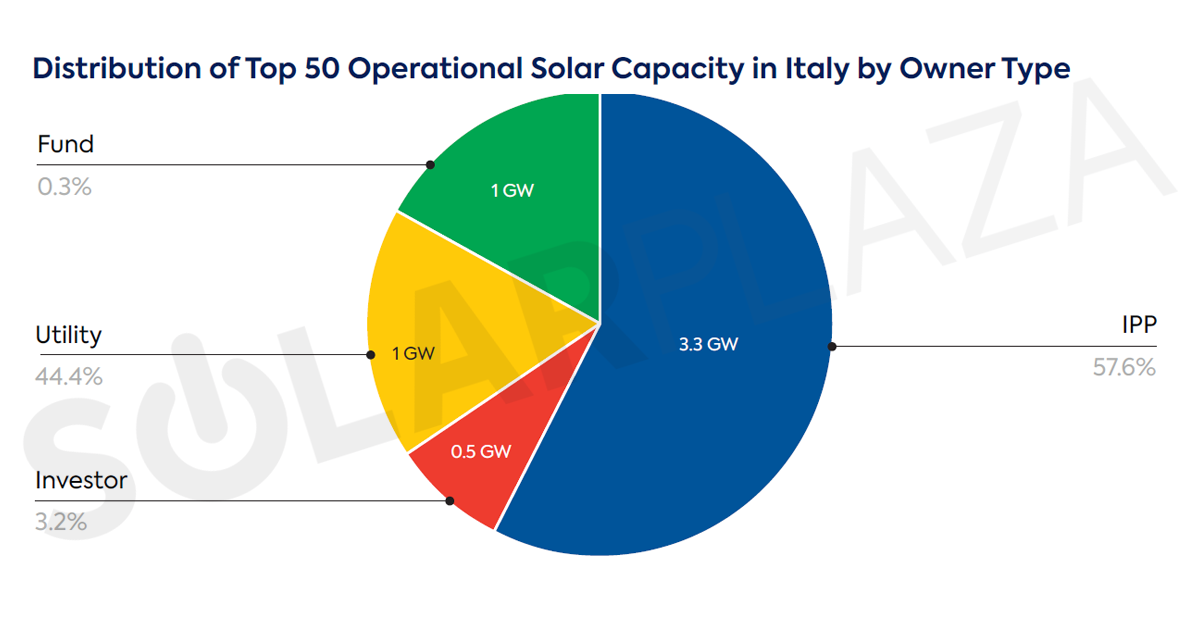

Independent Power Producers (IPPs) account for the largest share of operational capacity within the Top 50's Italian exposure, totaling approximately 3.3 GW. Utilities also hold a strong presence, collectively accounting for nearly 1 GW of capacity. Enel Green Power operates approximately 430 MW of this localized baseline, while Engie and Iberdrola also manage assets in the country. Institutional investors and specialized funds collectively manage more than 1.4 GW, with support from NextEnergy Group and several infrastructure-backed ownership vehicles.

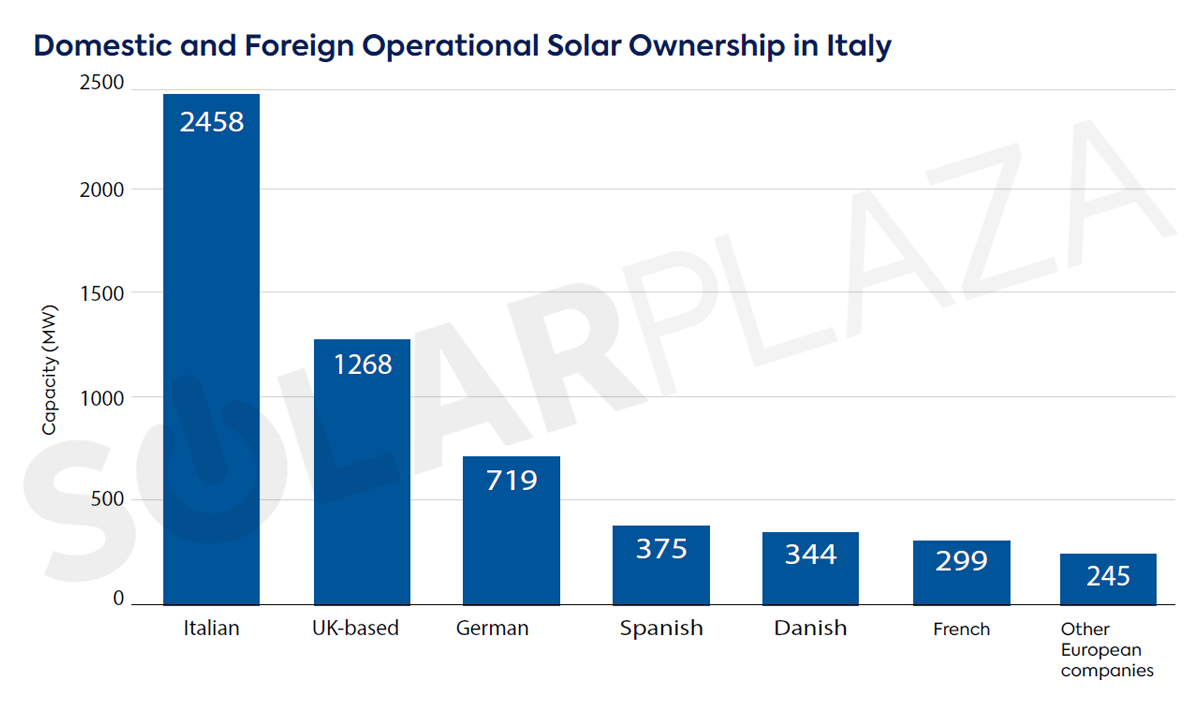

Domestic control remains low compared to other large continental markets, with Italian-headquartered organizations owning just 43.1% of the local ranked asset base. Foreign participation is highly diverse, led by UK-based asset managers with 1.3 GW and German operators with more than 700 MW, alongside significant contributions from Spanish, Danish, and French platforms. Conversely, Italian portfolio owners show an outward focus toward Spain, where they deploy 3.3 GW of capacity. This represents substantially more operational capacity than they collectively hold in their home market in our tracking, highlighting a strong financial connection between the two regions.

Entering complex merchant markets without benchmarking your operational efficiency against international platforms creates a substantial financial blind spot. Visit the main resource page today to access your free account and download the full report.