Europe's utility-scale solar asset ownership landscape is entering a highly competitive phase where scale, location, and operational strategy dictate financial survival. As asset owners face rising grid congestion and more frequent negative pricing events, understanding who controls the market and where the capacity sits is becoming a strategic necessity as we enter the next phase of solar asset ownership.

The latest data from the top 50 operating solar portfolios in Europe reveals massive consolidation and expansion. The cumulative operational capacity among the continent's largest owners has surged to 67.4 GW, up from 55.5 GW in the previous report. This means a select group of institutional players now controls approximately 15% of Europe's entire installed solar capacity.

To give you an immediate competitive edge, we compiled the definitive snapshot of the European asset landscape ahead of the Solarplaza Summit Asset Management Europe. This comprehensive report goes beyond development pipelines to map out true, retained operational ownership across the continent.

Below is a brief look at the core asset dynamics driving the European market.

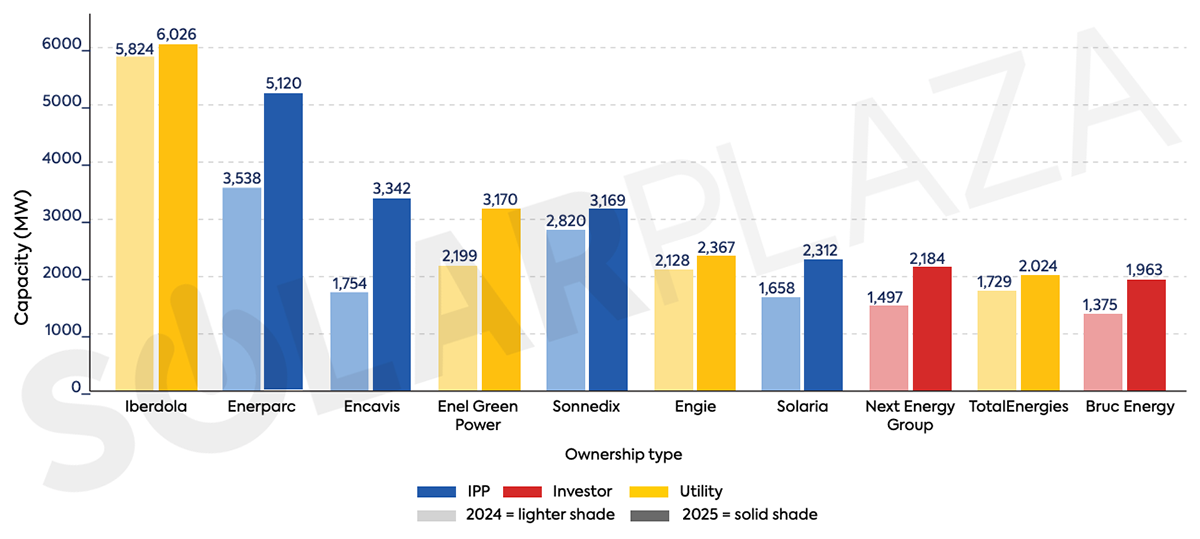

Top 10 operational solar portfolios capacities in 2024 vs 2025

The data shows that market control is concentrating heavily at the very top of the ranking.

-

The top 10 companies alone account for 31.7 GW of operational capacity, representing 47% of the total capacity in the top 50 ranking.

-

Integrated utilities and large independent power producers (IPPs) continue to lead the upper tier, with Iberdrola maintaining its position as Europe's largest operational owner at 6,026 MW, followed by Enerparc at 5,120 MW.

-

Admission to this top tier now requires a portfolio of nearly 2 GW of operational assets, illustrating the steep barriers to entry for achieving true continental scale.

-

Portfolio growth across the top 10 remains uneven, with players like Encavis and Enerparc recording the largest absolute capacity additions, while others maintain more stable, conservative growth trajectories.

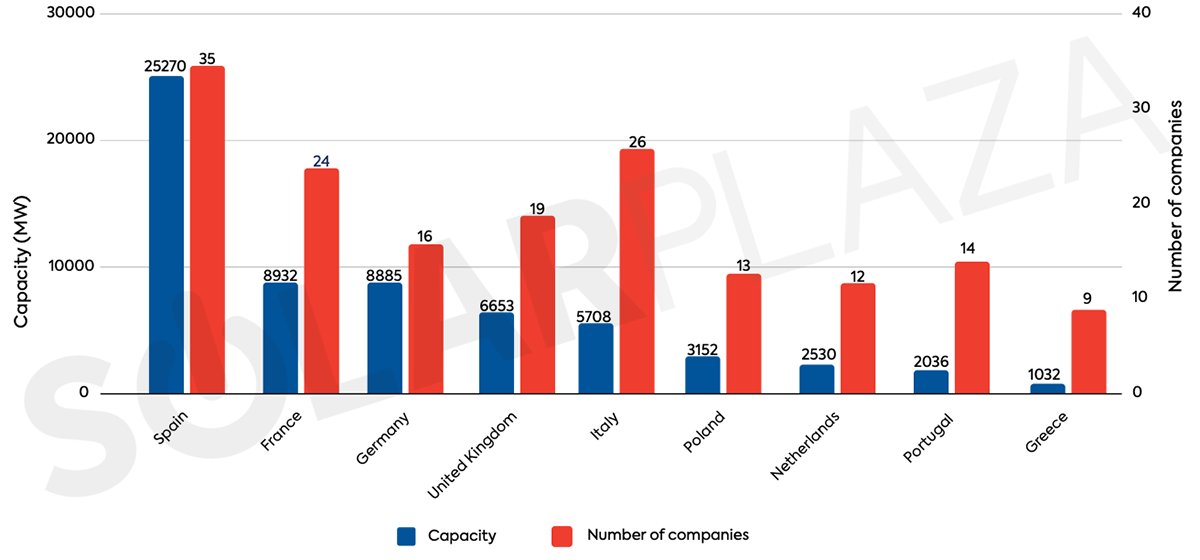

Geographic distribution of the top 50 across key European solar markets

Furthermore, the operational footprint detailed in the second graph highlights that while assets are spread across more than twenty countries, the physical capacity remains heavily concentrated in Western and Southern Europe.

-

Spain is Europe's primary operating market, hosting 25,270 MW of capacity across 35 portfolio owners.

-

Every company in the top 10 maintains operational assets in Spain, underscoring Spain's status as the central hub for utility-scale solar asset management.

-

France and Germany follow closely in the ranking, with each country hosting approximately 8.9 GW of capacity within the top 50.

-

The structural drivers of these top markets differ fundamentally: Germany's utility-scale segment remains highly fragmented, whereas France's is utility-led and domestically anchored.

Secure your strategic market map

Managing merchant price exposure, evaluating battery energy storage systems (BESS) integration, and optimizing revenue across multiple borders require deep data. Missing out on these asset trends means risking misaligned portfolio strategies and lost ROI in Europe's most lucrative markets.

Download the full white paper below to explore:

-

The complete top 50 portfolio rankings and ownership structures.

-

Detailed breakdowns of specialized ownership profiles across Spain, Germany, France, Italy, and the United Kingdom.

-

Critical operational trends regarding cross-border ownership and asset management diversification.