Ground-mounted solar, SDE++ scheme, and grid constraints

Author: Zsolt Szalay

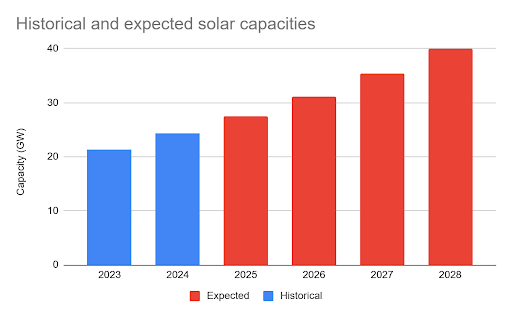

The Netherlands added 3.1 GW of solar capacity in 2024, a sharp decline from the 5 GW recorded in 2023. What's causing the slump? Our new article dives into the prospects for ground-mounted solar, the status of the SDE++ scheme, and the challenges and opportunities related to grid constraints.

Introduction

According to CBS data, the Netherlands added 3.1 GW of solar capacity in 2024, a sharp decline from nearly 5 GW in 2023.¹ This slowdown is primarily due to the collapse of the residential solar market, which shrank by nearly 70%.

Despite this setback, SolarPower Europe projects that the Netherlands will reach 40 GW of operational solar capacity by 2028, requiring an average of 4 GW of annual additions over the next four years.² Grid operators estimate that solar capacity could reach 42-76 GW by 2030, while the National Energy Plan (Nationaal Plan Energiesysteem) forecasts over 50 GW by the end of the decade.

Source: CBS & SolarPower Europe

Electricity mix

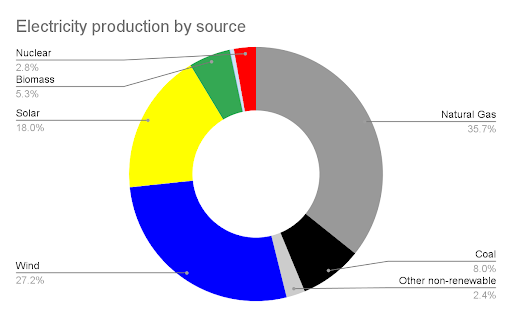

The Netherlands has reached a historic milestone in its energy transition. In 2024, for the first time, renewable sources generated more electricity than fossil fuels and nuclear power combined. According to CBS, wind, solar, biomass, and hydropower produced 61.4 TWh, accounting for 51% of the country’s total electricity generation.³ This marks a strategic shift toward reducing fossil fuel dependence while advancing both national and European climate commitments.

The data show a 4% decline in fossil fuel electricity production, while renewable energy generation increased by 10% compared to 2023. Wind energy saw the largest growth, rising 13% to 32.7 TWh, while solar generation grew by more than 10%, reaching 21.6 TWh.

Source: CBS

Ground-mounted solar

Despite an increase in ground-mounted solar installations compared to 2023, the sector is grappling with major obstacles.² For example, permitting remains a significant hurdle. In 2023, the Dutch government introduced new spatial planning regulations to address concerns over land use. These rules, which restrict the types of solar parks that can be developed, were largely adopted at the provincial level, creating widespread uncertainty. As a result, securing permits for projects that lack a multifunctional purpose has become increasingly difficult.

Grid congestion presents another challenge, but it has also shaped new trends. To bypass long waiting periods for grid expansion, more developers are opting for local solar parks that feed directly into regional grids. In response, communities are urging provincial governments to approve solar projects near new residential developments, where local demand is high.

Meanwhile, congestion management efforts are starting to yield results. The mandatory participation of all installations above 1 MW in congestion programs has gradually freed up grid capacity, allowing more projects to connect. Additionally, new standardized contracts for flexible grid connections are being introduced, offering shorter wait times.

The battery storage market is now gaining momentum. A key driver is the increasing mismatch between supply and demand, as many residential solar systems fail to adjust to market dynamics, leading to low capture prices. This gap presents a major opportunity for solar developers. By integrating storage solutions, the value of solar generation can be significantly enhanced. Furthermore, with natural gas prices increasingly setting electricity rates during off-peak hours, shifting solar consumption to different times of the day is becoming a more attractive business case. To accelerate this shift, the government has announced a €300 million subsidy scheme to support co-located solar & storage projects.

SDE++

In February 2025, the Ministry of Climate Policy and Green Growth (Ministerie van Klimaat en Groene Groei - KGG) announced that the SDE++ subsidy program for 2025 would be open for applications from 7 October to 8 November, with a total budget of €8 billion.⁴ This program remains a crucial financial mechanism supporting the development of large-scale renewable energy projects, particularly solar energy.

Grid congestion presents another challenge, but it has also shaped new trends. To bypass long waiting periods for grid expansion, more developers are opting for local solar parks that feed directly into regional grids. In response, communities are urging provincial governments to approve solar projects near new residential developments, where local demand is high.

The Dutch solar industry welcomed the improvements made to the scheme. The 2025 SDE++ round expands opportunities for Agrivoltics and solar heat. A notable change is the inclusion of vertical solar panels, which will benefit Agrivoltaics developers and provide farmers with sustainable energy solutions and an additional source of income. Another significant addition is the introduction of a new category for large-scale PVT (Photovoltaic-Thermal) with WKO (Warmte-koude opslag, Aquifer Thermal Energy Storage - ATES), which enhances heating network potential by integrating solar and thermal storage solutions. Furthermore, solar facades have been added to the subsidy framework, opening new possibilities for high-rise buildings, where facade surfaces often provide more space for solar generation than rooftops.

A further positive development is that, from 2025 onward, all ground-mounted solar projects will be required to be nature-inclusive, ensuring that solar farms contribute not only to renewable electricity production but also to biodiversity conservation.

One of the key challenges facing the sector is the increasing number of hours when electricity prices turn negative, largely due to the slow progress of electrification and demand flexibility. The Netherlands Environmental Assessment Agency (Planbureau voor de Leefomgeving - PBL) and the ministry are addressing this issue by introducing a correction factor in the subsidy calculation that accounts for negative electricity price hours. Holland Solar welcomes this initiative but urges the government to extend support to existing projects facing financial risks from price volatility.

Concerns also remain regarding future funding, as uncertainty looms over the 2026 SDE++ round. Industry groups Holland Solar and NedZero are calling on the government to provide clarity soon, as financial risks for large-scale solar projects remain high. While the sector aims to become subsidy-free, investors still require certainty to proceed with projects.

Grid investments - How much is needed?

The Dutch electricity grid is experiencing severe congestion, creating challenges for businesses, renewable energy developers, and grid operators. To maintain its leading position in the energy transition, the Netherlands must invest heavily in grid infrastructure.

On 7 March 2025, the Interdepartmental Policy Research (Interdepartementale beleidsonderzoeken - IBO) released a report that examines the investment requirements for the Dutch electricity infrastructure until 2040. According to their findings, the Netherlands faces a triple challenge in its energy transition: meeting CO2 reduction targets, reducing dependence on unreliable energy imports, and maintaining affordable energy costs for consumers and businesses. To address these issues, a large-scale grid expansion is required, with significant economic and social implications.

Currently, over 20,000 connection requests remain on hold, delaying business growth and residential expansion.⁵ Studies estimate that grid congestion costs society between €10 billion and €40 billion annually. To alleviate this, the IBO projects a total investment of €195 billion between 2024 and 2040, averaging €11 billion per year. Of this, €88 billion is set for offshore wind grid connections, while €107 billion is allocated for onshore expansion. These upgrades aim to enhance energy security and economic resilience but will significantly raise energy costs. By 2040, network tariffs could increase from 4.8% to 6.7% annually, with household grid fees rising from €400 in 2024 to €1100 in 2040.

While the IBO report emphasizes the need for large-scale investment, Holland Solar, NedZero, and Energy Storage NL (ESNL) argue that such an expensive expansion may not be necessary.⁶ They suggest that enhancing electrification, demand flexibility, and storage could cut grid costs by more than 20%, as indicated by government findings. Instead of extensive infrastructure expansion, these groups advocate for better utilization of existing grid capacity.

Wijnand van Hooff, General Manager at Holland Solar, highlights that locally produced renewable electricity is far more cost-effective than relying on imported natural gas and oil. Similarly, Maarten van den Heuvel, Chairman at ESNL, stresses that energy storage, including electricity, heat, and hydrogen, plays a vital role in keeping the energy system affordable. Research by Kalavasta supports this claim, showing that integrating storage solutions could yield substantial cost savings by 2040.

Industry groups also call for a comprehensive strategy to optimize the grid’s flexibility. They propose measures such as demand-side management, energy storage, and conversion technologies to better align production with consumption, ultimately reducing the need for large-scale grid expansion.

In conclusion, while acknowledging the need for investment in the electricity grid to meet rising demand, Holland Solar, NedZero, and ESNL argue that strategic enhancements in system flexibility and energy storage can substantially lower the projected costs, challenging the necessity of the €195 billion investment suggested by the IBO report.

Closing words

The Netherlands is at a pivotal moment in its energy transition. While renewable energy generation has surpassed fossil fuels for the first time, and solar capacity continues to expand, grid congestion and permitting challenges threaten to slow further progress. Despite ambitious solar growth projections, the bottlenecks in infrastructure and regulatory uncertainty pose significant risks to long-term development.

Investment in grid expansion is critical, yet industry groups argue that a smarter approach could reduce the need for massive infrastructure spending. The debate surrounding the €195 billion grid investment plan highlights the need for balanced solutions that enhance capacity while ensuring cost efficiency for consumers and businesses.

Policy support through SDE++ subsidies remains a key driver of solar deployment, particularly for Agrivoltaics, PVT, and solar facades. The 2025 SDE++ round introduces important improvements, addressing financial risks and negative electricity pricing. However, uncertainty over the 2026 budget raises concerns about the sector’s long-term stability.

To support the industry in navigating this complex and evolving landscape, the Solarplaza Summit The Netherlands – Future of Solar Revenues will take place in Amersfoort on 17 June 2025. This strategic one-day conference is designed to explore the future of the Dutch solar market, offering attendees crucial insights into regulatory shifts, innovative financial models, and adaptive market strategies. The event will equip investors, developers, IPPs, and energy professionals with the knowledge and tools needed to succeed in a rapidly transforming energy sector.

Ultimately, the success of the Dutch energy transition will depend on how effectively policymakers, grid operators, and industry stakeholders collaborate to resolve infrastructure constraints, optimize energy distribution, and implement forward-thinking policies. Without swift action to modernize the grid and improve regulatory clarity, the country risks missing its renewable energy targets despite strong market momentum. The coming years will be crucial in determining whether the Netherlands can sustain its leadership in the renewable energy revolution.

Sources

1 CBS (2025) Renewable electricity; production and capacity. Retrieved from https://opendata.cbs.nl/statline/#/CBS/en/dataset/82610ENG/table?ts=1741782570121

2 SolarPower Europe (2024) EU Market Outlook for Solar Power 2024-2028. Retrieved from https://www.solarpowereurope.org/insights/outlooks/eu-market-outlook-for-solar-power-2024-2028

3 CBS (2025) Electricity balance sheet; supply and consumption. Retrieved from https://opendata.cbs.nl/#/CBS/en/dataset/84575ENG/table?ts=1673608315537

4 Holland Solar (2025) Reactie Holland Solar op PBL-eindadvies SDE++ 2025. Retrieved from https://www.hollandsolar.nl/actueel/reactie-holland-solar-op-pbl-eindadvies-sde-2025.html

5 Rijksoverheid (2025) Schakelen naar de toekomst. IBO Bekostiging Elektriciteitsinfrastructuur. Retrieved from https://www.rijksoverheid.nl/documenten/rapporten/2025/03/07/schakelen-naar-de-toekomst-over-bekostiging-elektriciteitsinfrastructuur

6 NedZero (2025) First reaction to IBO research: investment of 200 billion is far from necessary. Retrieved from

https://nedzero.nl/en/news/first-reaction-to-ibo-research-investment-of-200-billion-is-far-from-necessary