Agrivoltaics is rapidly gaining traction across Europe, promising a powerful combination of renewable energy generation and agricultural resilience. With growing political support and over 200 projects already in operation, the concept is moving beyond pilots into real market deployment.

Despite rising interest, agrivoltaics still faces a fragmented regulatory landscape, unclear market rules, and growing pressure to prove its value beyond electricity generation. As more projects enter development, the gap between ambition and practical implementation is becoming harder to ignore.

In fact, the market is now confronting three critical realities: policy support does not guarantee clarity, agriculture can no longer be treated as secondary, and not every project delivers a true win-win outcome.

Key insights from the article:

- Why policy momentum is outpacing regulatory clarity across Europe

- How fragmented frameworks are slowing down project development

- Why agronomy is becoming a core requirement, not an add-on

- The economic trade-offs behind agrivoltaic projects

- What separates successful projects from those that struggle

Access the full analysis

Create an account or log in to dive deeper into the realities shaping agrivoltaics in Europe and what it takes to make projects viable in today’s evolving market.

Introduction

Agrivoltaics is recognized as a practical way to combine renewable energy production with continued agricultural use, while also helping farmers respond to climate pressure, land scarcity, and energy price volatility. A 2023 European Commission (EC) research suggests that just 1% of Europe’s agricultural land could host roughly 944 GW of agrivoltaics capacity, while more recent industry and policy sources point to growing political recognition and more than 200 agrivoltaic projects already operating across Europe (EC, 2023) (AgriSolar, 2025). This shows that agrivoltaics has moved well beyond the pilot stage in terms of visibility and ambition.

But growth in visibility should not be confused with maturity. Despite stronger policy attention and a growing pipeline of projects, agrivoltaics in Europe still develops in a highly uneven landscape. Recent policy mapping shows that only a limited number of EU member states have introduced a legal definition of agrivoltaics, while permitting land-use treatment, Common Agricultural Policy (CAP) eligibility, and support schemes still vary considerably across markets (SolarPower Europe, 2025) (Alves et al., 2026). In other words, the concept is gaining traction faster than the rules are converging around it.

That mismatch is exactly what makes agrivoltaics such an important topic for the market right now. The challenge is no longer whether it has potential, but what it actually takes to make projects work in practice. As newer policy and academic sources suggest, success depends less on the promise of dual use alone and more on the quality of the regulatory framework, the credibility of the agricultural model, and the ability to demonstrate real value beyond electricity generation (Alves et al., 2026) (Vezzoni, 2025).

This is where the conversation becomes more interesting. While agrivoltaics is often presented as a win-win solution, the reality on the ground is more complex. Europe has made progress since the EC’s earlier assessment. However, many of the structural issues identified, such as fragmented regulation, unclear project classification, and uneven support mechanisms, still shape the market today (EC, 2023) (SolarPower Europe, 2025).

The market is now mature enough to face the following three hard truths: political momentum does not automatically create project clarity, agricultural value cannot remain an afterthought, and not every agrivoltaics project is a genuine win-win.

Hard Truth #1: Policy momentum does not equal market clarity

At first glance, agrivoltaics appears to be gaining strong political traction throughout Europe. Recent EU-level strategies now recognize the role of solar in agriculture, highlighting its potential to improve farm resilience, increase income stability, and contribute to energy security (AgriSolar, 2025) (EC, 2026). This indicates a considerable shift from just a few years ago, when agrivoltaics was still largely treated as a niche or experimental concept.

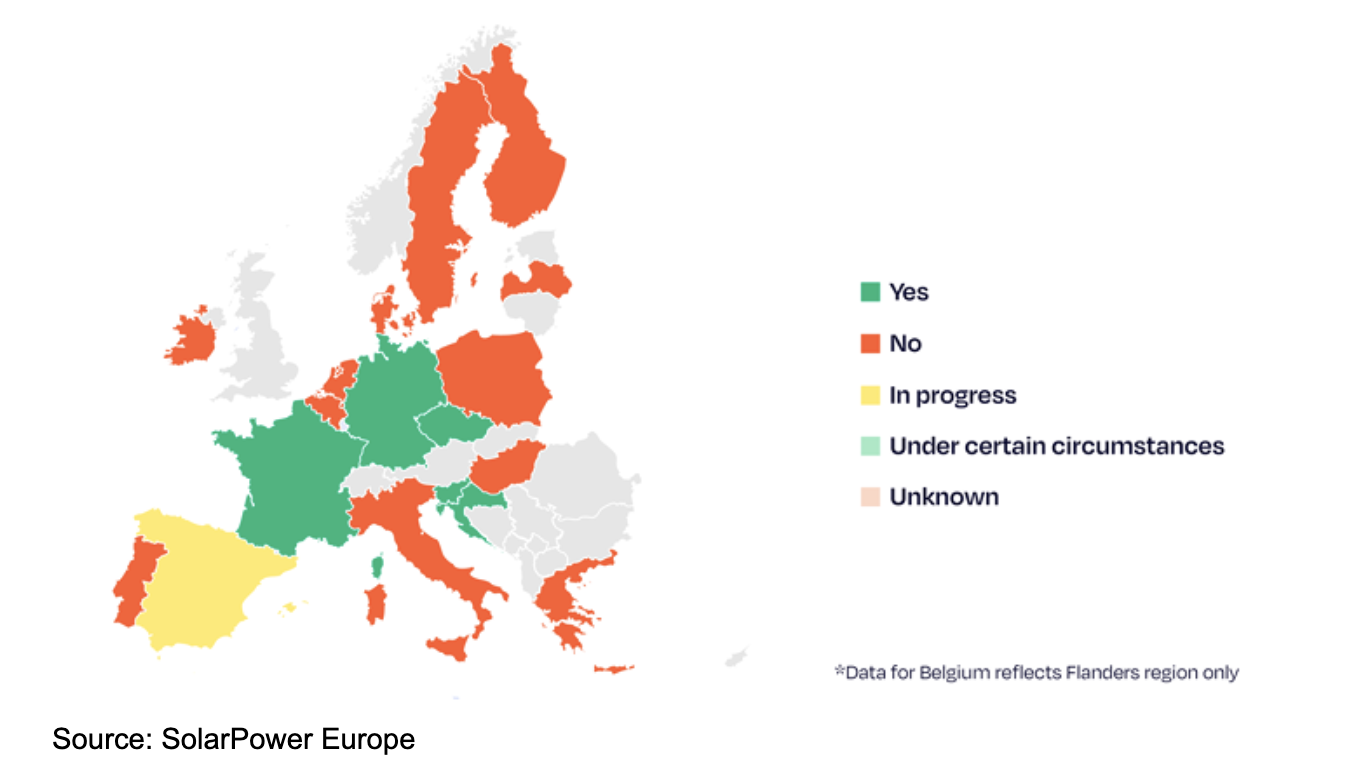

However, this rising recognition has not yet translated into a coherent and predictable market environment. Across Europe, the regulatory landscape remains fragmented. Only a limited number of member states (Czechia, Croatia, France, Germany, and Slovenia) have introduced a clear legal definition of agrivoltaics, while others are still in the process of defining what qualifies as dual-use solar (SolarPower Europe, 2025) (Alves et al., 2026). As a result, similar projects may be treated very differently depending on the country, or even the region, in which they are developed.

Presence of a legal definition for agrivoltaics

This lack of alignment extends well beyond definitions. Permitting procedures, land-use classifications, and eligibility for agricultural subsidies under the CAP still vary widely across the countries. In some countries, agrivoltaic systems are recognized as compatible with agricultural land use, while in others they face restrictions, unclear zoning rules, or lengthy approval timelines. Even where support mechanisms exist, such as dedicated auctions or subsidy schemes, their implementation is often inconsistent or still pending regulatory approval (Leadvent, 2026).

The EC’s 2023 research already identified fragmented regulation and unclear frameworks as key barriers to scaling agrivoltaics (EC, 2023). What has changed since then is not the nature of the problem, but its urgency. As more projects enter development pipelines and capital begins to flow into the sector, these inconsistencies are becoming real bottlenecks rather than theoretical limitations (Alves et al., 2026). They are now directly impacting project timeframes and bankability.

For developers, this creates a fundamentally different playing field compared with conventional solar. Success in agrivoltaics is no longer about securing land and grid access. It requires managing a complex and evolving regulatory environment in which definitions, requirements, and incentives remain in flux. In practice, this means that understanding regulatory frameworks has become just as critical as technical design or financial structuring.

Hard Truth #2: Agronomy is no longer optional

One of the biggest misconceptions about agrivoltaics is that it is simply a solar project with crops or livestock added underneath. In reality, the agricultural component is a central theme to whether a project is approved, financed, and ultimately successful (EC, 2023) (Alves et al., 2026). Agrivoltaics operates at the intersection of two sectors with very different priorities, and harmonizing them in practice is far more complex than it appears on paper.

In Europe, several national frameworks now require developers to demonstrate that agricultural activity remains the primary land use and that crop yields or farming functions are preserved (SolarPower Europe, 2025) (Leadvent, 2026). In countries like France and Italy, eligibility for incentives or permits is directly linked to maintaining agricultural productivity or delivering defined “agricultural services,” like crop protection or improved resilience to climate conditions.

At the same time, the evidence base behind agrivoltaics is still developing. While studies show that well-designed systems can improve land-use efficiency and even strengthen crop resilience under certain conditions, results are highly site-specific (Alves et al., 2026) (Vezzoni, 2025). Factors such as crop type, system design, shading patterns, and local climate all influence outcomes, making it difficult to generalize performance among projects. This uncertainty increases the importance of pilot projects, monitoring, and agronomic validation early in the development process.

This lack of evidence is what many projects struggle with. Without credible agronomic data, projects may encounter delays in permitting, challenges in securing financing, or resistance from farmers and local stakeholders (EC, 2023). In some cases, poorly designed projects have prioritized energy output at the expense of agricultural viability, leading to skepticism around whether agrivoltaics truly delivers on its “dual-use” promise (Alves et al., 2026).

As a result, the role of agronomy in agrivoltaics is shifting from a supportive consideration to a core requirement. Developers are expected to work closely with farmers, integrate agricultural expertise into project design, and provide long-term evidence of performance. In practice, this means that successful agrivoltaic projects are co-developed with agriculture at their core.

Hard Truth #3: Not every project is a win-win

Agrivoltaics is often presented as a straightforward win-win solution. One that simultaneously results in increased renewable energy generation, more resilient agriculture, and better land use. While this vision is compelling and, in some cases, achievable, the reality is more complex. Whether an agrivoltaic project delivers on that promise depends heavily on local conditions, project design, and the wider economic and regulatory context (Vezzoni, 2025).

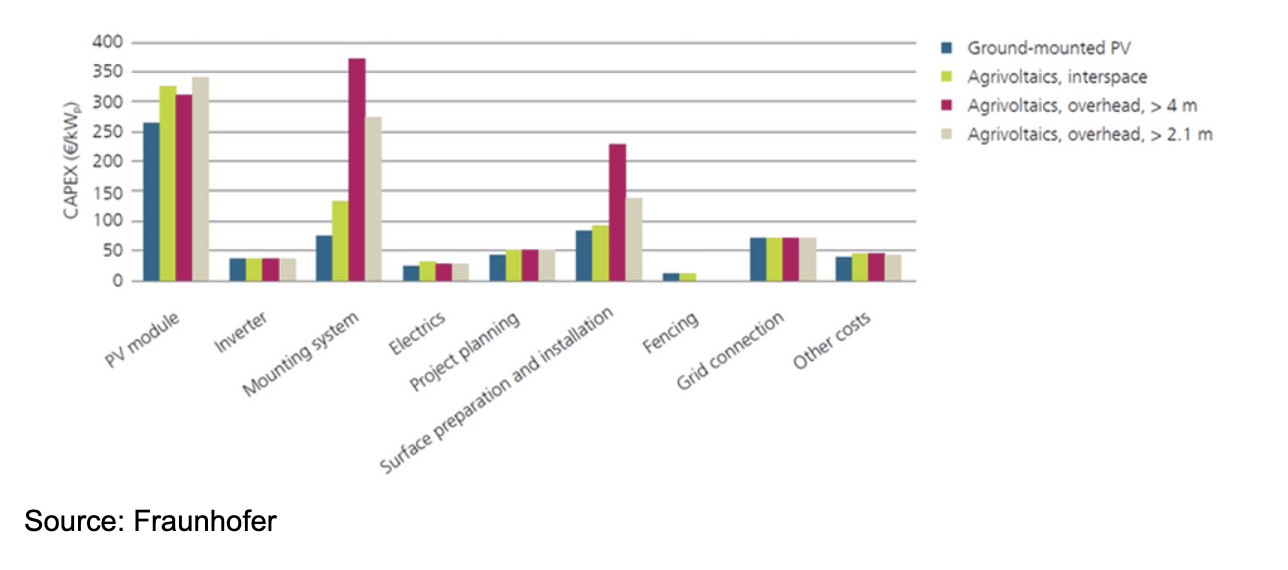

From an economic perspective, agrivoltaics does not automatically outperform conventional solar. While it can improve overall land-use efficiency by combining energy and agricultural production on the same site, it also comes with significantly higher upfront costs due to more complex structures, installation requirements, and system design. Studies indicate that capital expenditures can be substantially higher than standard ground-mounted PV, and in many cases, the levelised cost of electricity remains higher as well. These factors make project viability more sensitive to subsidies, electricity prices, and policy support mechanisms.

Estimated CAPEX for ground-mounted PV and three different agrivoltaic systems

At the same time, the broader market environment is becoming more challenging. As solar penetration increases across Europe, price cannibalization effects are already putting pressure on revenues, particularly during peak generation hours. For agrivoltaic projects, this introduces an additional layer of uncertainty to the business case, especially in the absence of long-term support schemes or stable power purchase agreements.

Beyond economics, agrivoltaics also introduces new trade-offs around land use, ownership, and value distribution. While solar leasing can greatly increase income for landowners, it may also drive up farmland prices and create additional pressure on farmers who rely on leased land. Is it the farmers, developers, or large energy companies with the resources to scale projects who ultimately benefit from agrivoltaic project development?

All of these challenge the idea that agrivoltaics is inherently a win-win solution. In practice, outcomes are highly context-specific. Well-designed projects in supportive regulatory conditions can deliver clear benefits for both energy production and agriculture (Alves et al., 2026) (Vezzoni, 2025). But without careful alignment between policy, project design, and local agricultural realities, agrivoltaics risks reproducing the same tensions it aims to solve between land use, economic value, and long-term sustainability.

Conclusion

Agrivoltaics has clearly moved beyond the experimental phase. Political recognition is increasing, project pipelines are growing, and the role of solar in agriculture is now part of Europe’s energy and farming strategies.

What becomes clear is that success in agrivoltaics now depends on navigating fragmented regulatory frameworks, integrating agriculture as a core component of project design, and building projects that are economically viable in a rapidly changing energy market. While progress has been made since the earlier EC assessments, many structural challenges remain and are becoming more visible as projects scale up.

For developers, investors, and policymakers, this means that agrivoltaics is entering a more demanding phase. The opportunity is still significant, but so is the complexity. Understanding what makes projects succeed or fail in practice is becoming critical for anyone looking to position themselves in this space.

These realities will be explored further during the panel ‘Why Agri-PV Projects Fail or Succeed: A Country-by-Country Reality Check’, taking place at the Solarplaza Summit Agri-PV Europe on 3 June 2026 in Paris, where industry experts will discuss how agrivoltaic development differs across Europe and what it takes to build viable projects in today’s market.

Sources

EC (2023) Overview of the potential and challenges for Agri-Photovoltaics in the European Union. Retrieved from https://publications.jrc.ec.europa.eu/repository/handle/JRC132879

AgriSolar (2025) EU Farming Strategy recognises the role of solar for first time. Retrieved from https://agrisolareurope.org/article/eu-farming-strategy-recognises-the-role-of-solar-for-first-time/

SolarPower Europe (2025) Agrisolar Policy Map. Retrieved from https://www.solarpowereurope.org/press-releases/new-report-solar-power-europe-launches-agrisolar-policy-map-to-guide-eu-strategy

Alves, A., da Costa, E.M. & Sirnik, I. (2026) The policy landscape of agrivoltaics: a systematic review. Retrieved from https://link.springer.com/article/10.1186/s13705-025-00555-7

Vezzoni, R. (2025) Farming the sun: the political economy of agrivoltaics in the European Union. Retrieved from https://link.springer.com/article/10.1007/s11625-024-01601-7

EC (2026) Agrivoltaics: accelerating Europe’s decarbonisation while safeguarding land, food production and energy security. Retrieved from https://sustainable-energy-week.ec.europa.eu/news/agrivoltaics-accelerating-europes-decarbonisation-while-safeguarding-land-food-production-and-energy-2026-03-23_en

Leadvent (2026) Policy Frameworks Supporting AgriVoltaics Growth in the EU. Retrieved from https://www.leadventgrp.com/blog/policy-frameworks-supporting-agrivoltaics-growth-in-the-e