Despite the strains the economy suffered as a result of the fall of oil prices, Nigeria might gain some consolation due to its changing regulatory framework meant to support solar energy. To fully understand the inherent characteristics of the Nigerian solar market, Solarplaza organized the webinar: Nigeria's Solar Market: Opportunities and Challenges in an Evolving Landscape. This webinar was a preparation for The Solar Future Nigeria, a 2-day conference taking place in Lagos on 25-26 April 2017. 200+ executives will gather and connect to discuss the challenges and opportunities that lie in the immediate future for Nigeria’s solar Power Market.

Assessing Nigeria’s economic and energy situation

“Nigeria’s population will add 80 million people and double its GDP output by the year 2030”

Nigeria is not only the most populous country in Africa, home to 180 million people in 2015, but it has also overtaken South Africa as the largest economy in the region, with a GDP of $480 billion. It is also estimated that Nigeria’s population will add 80 million people and double its GDP output by the year 2030. In order to achieve such growth however, Nigeria would require a substantial increase and improvement of its current energy situation to meet the heaping demand.

“Nigeria’s energy situation is far from ideal for several reasons” claims Godwin Aigbokhan, the executive secretary of the Renewable Energy Association of Nigeria (REAN), the local umbrella committee for renewable associations. “As a result of low investment, high corruption, poor planning and inadequate maintenance, the status of Nigeria’s on-grid sector is rather unfavorable to say the least.”

The electrification rate in the country amounts to a mere 126 kWh per capita which not only is miniscule compared to developed countries but also lags behind regional values. The availability of grid-supplied electricity isn’t in great shape either, as electricity was only supplied for 6.2 hours on average per day, between 2013 and 2015. Furthermore, stemming from the substandard condition of the grid system, only 25-30% of the total installed capacity is actually readily available for consumers, amounting to 12 GW of true grid power capacity. Because of the imperfect infrastructural situation, self-generation is a common phenomenon, amounting to 8-14 GW of total energy consumption.

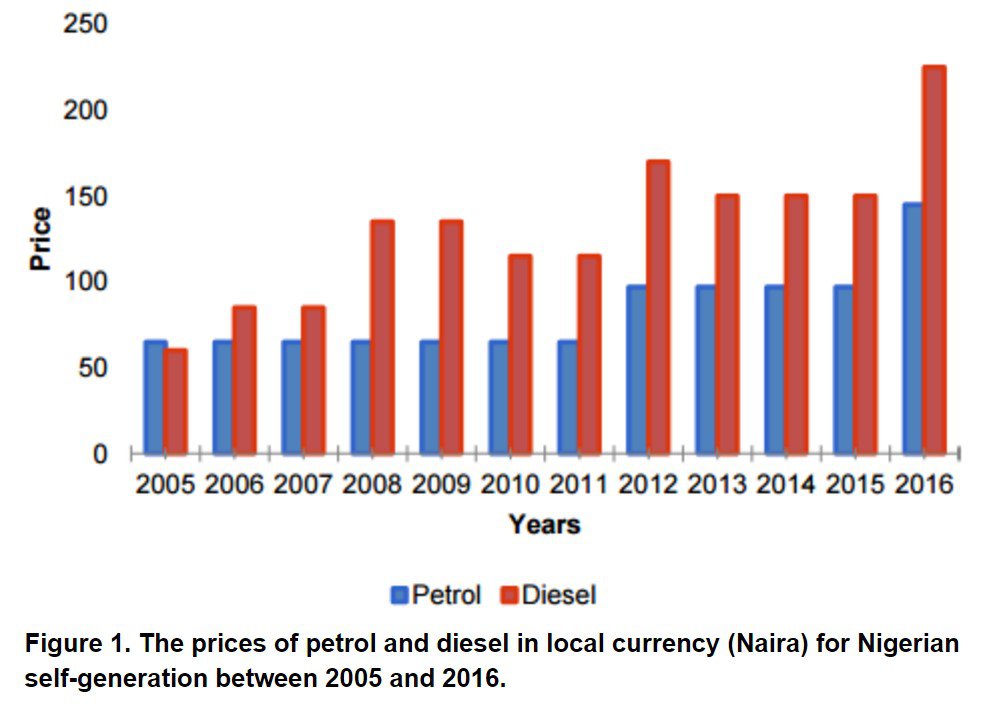

The core issue with self-generation as it is right now, however, does not lie in the main grid’s underutilization, but rather in the overutilization of costly fossil fuel generators. Diesel and petrol generators are the most common self-electrification methods in Nigeria and place a considerable financial burden on consumers. The rise in prices depicted in Figure 1 gives insights into how pressing of an issue it is for the country to diverge from the abovementioned sources. To put these prices into perspective: the local price of generation from solar energy is estimated to be 15.5 Naira (at the time of the article the official exchange rate is 1 Naira = 0.0032 USD).

“Considering electricity generation with diesel was projected to increase to $16.4 billion by 2016, energy generation constitutes an immense financial burden on Nigerians.”

The use of petrol and diesel generators is, by no means, inherent to the residential sector. It is estimated that 17 million SMEs rely on generators for an average of 8 hours/day for 25 days/month. Generators accounted for 80% of the total $5.2 billion fuel costs that was spent in 2012. Considering that this value was projected to increase to $16.4 billion by 2016, energy generation constitutes an immense financial burden on Nigerians.

Nigerian solar sector at a glance

The future of Nigeria need not to be as gloomy as the current numbers would suggest. The light of hope comes, quite literally, from the country's outstanding solar potential. Global Horizontal Irradiation levels range from 3.5 kWh/m2/day in coastal regions to about 9.0 kWh/m2/day in Northern borders, as pointed out by Mr. Aigbokhan. The government, in an attempt to exploit this potential, has put forth a wide range of policies in recent years. Such policies include a variety of tax incentives on renewable energy related investments as well as targets to increase rural electrification and the share of renewable energy sources in Nigeria’s current energy mix. With such actions the country is hope to advance the current state of its solar sector.

“To get a clear picture of where the local solar sector is headed, it is imperative to take the evolution of general Nigerian energy sector into account” emphasizes Erabor A. Okogun the CEO of Middle Band Solar One. In the initial phases, Nigeria mainly sourced power from hydroelectric sources through publicly owned power plants. Consecutively, Nigeria commenced the adoption of fossil fuel plants to widen the energy mix and increase energy security. This phase saw the emergence of privatized power with increased emphasis on the bankability of power projects. Since climate change became a central issue in the power sector’s design, cleaner sources of energy were starting to enjoy priority. As a result, following the power sector’s trend, privately owned solar projects are proving to be a good fit with the country’s needs.

“A shift from unsolicited tenders to solicited ones could well change the future energy landscape.”

As a pioneer, Mr. Okogun took part in the project development of the largest sub-Saharan PV plant, the Middle Band Solar One project. His involvement in the project resulted in unique, practical insights into the dynamics of solar project development which boiled down to a scheme of establishing Independent Power Producer (IPP) agreements (Figure 2). The 120MW project commenced with contacting local, publicly owned liability company, Nigerian Bulk Electricity Trade (NBET) in 2012. Mr. Okogun highlighted that the involvement of international financiers in the very early phases of the project timeline, roughly 1-2 years after initial talks, was essential in the project’s success. The next major step was obtaining the licensing required for the project. This process started in September, 2014 and ended with the acquisition of licenses in December, 2015 taking slightly longer than a year.

After the proper licenses were obtained and the project got financial backing, the negotiation of the Put Call Option Agreement (PCOA) and Power Purchase Agreements followed. Whereas the latter has seen consensus after a 2-year-long negotiation, the PCOA is still in negotiation, after two years, preventing the project from reaching financial close. The construction is expected to take 15 months - however, the project can be connected to grid incrementally by 5-10 MW at a time. Mr Okogun highlights meticulous project development and sector bankability as key success factors in bringing solar projects to life.

Off-grid sector: powering the rural and the remote

The development of microgrid and off-grid sectors are also crucial aspects the Nigerian government must tend to in order to facilitate the country’s economic development. The weak grid infrastructure and the approximated 100 million inhabitants without access to grid present a huge potential for non-grid applications. “Despite the clear demand however, there are several issues that have to be kept in mind for both micro-grid and off-grid plants” urges Femi Adeyemo, CEO of Arnergy, a company that specializes in designing solar energy systems in Africa.

One of the problems with micro-grid PV plants presents itself from the investor’s perspective. While long-term capital would be essential to establish such projects, Nigerian commercial banks do not provide financial means to overcome this obstacle. Simultaneously, heavy local currency volatility was another discouraging factor for investors recently. On the buyer's side it is a considerable matter of concern that prices of electricity sourced from microgrids tend to be higher than that off the grid. “Even so, with higher risk comes more opportunities for less risk-averse investors” says Mr. Adeyemo.

Similarly, there are issues that burden the development of off-grid applications such as PAYGO and roof-top installations. Energy theft remains to be a recurring problem. However, with employment of new technologies, these risks can be significantly mitigated. Regarding the business model adopted for off-grid sales, it is still not clear whether energy as a service or leasing to own will be the prevailing form as neither have managed to capture significantly bigger market share compared to the other. An encouraging sign for the off-grid sector, on the other hand, comes in the form of direct governmental investment into different applications amounting to nearly USD 30 million.

Overall, the need for solar PV energy is clearly present in the Nigerian market and this need will potentially increase in the future. While significant risk factors have limited investor interest in the country, the government’s adoption of IPPs should act to facilitate projects. Likewise, direct governmental support in the sector is intended to promote the off-grid sector. Judging by the projected growth in demand and the fit solar PV offers in addressing current issues, Nigeria will undoubtedly continue to increase its attractiveness towards investors looking to solidify the country’s solar power potential.