White Paper

1 September 2015

Estimated reading time: 10 min

India - A Renewed and Resurgent National Solar Mission

I want to kill 10 birds with one stone!

‘I want to kill 10 birds with one stone!’ aptly describes the aspirations, targets and determination of Hon’ble Minister for Power, Coal and Renewable Energy, Shri Piyush Goyal when it comes to resolving India’s power sector problems. This statement is turning out to be prophetic – at least as far as solar is concerned.

In 2009, on the eve of the Copenhagen Summit of UNFCCC, when the then Prime Minister Manmohan Singh launched the National Solar Mission, with a target of 20,000 MW by 2022, solar industry veterans in India couldn’t believe that change could be ushered so fast. This groundbreaking move aligned an almost three-decade-old Ministry for New and Renewable Energy (perhaps the first independent ministry of its kind anywhere in the world) with the much bigger Power Ministry by setting RPOs (renewable purchase obligations) and signing of long-term PPAs (power purchase agreements) for export of solar power into the grid.

The Master Stroke – Power, Coal and Renewable Energy under one Minister

Almost 5 years later, in 2014, the new government led by Prime Minister Modi took over. Modi was a known champion of solar, with almost 1000 MW of solar installed in Gujarat between 2010-11 when he was the chief minister – more than in the rest of the entire country. While the credit for aligning solar with the power sector goes to Mr Manmohan Singh, the master stroke, played by Mr Narendra Modi, was to place all of the portfolios for coal and renewable energy and power under a young and energetic minister. Prime Minister Modi and his dynamic Power Minister Mr Piyush Goyal took time to consult the bureaucrats and industry stakeholders before setting the new target of 100,000 MW by 2022 – a fivefold increase which left the bureaucrats groaning and even the die-hard solar veterans gasping in disbelief. This is what is known as the ‘Big Hairy Audacious Goal’ – BHAG – a goal with a serious wow factor that stretches people to imagine and strive hard.

Industry analysts and consultants, however, came forth with various comments, analyses and charts showing why and how 100,000 MW would not be possible. Even as late as June 2015, Bridge to India released the India Solar Handbook wherein they estimated that India may achieve about 35 or 38 GW only. But a BHAG is just that: a rallying cry intended to inspire and bring about collective action to achieve the goal by gathering momentum.

The term BHAG was coined by James Collins and Jerry Porras in their classic management book Built to Last – Successful Habits of Visionary Companies which gave examples of companies such as HP and Sony that had articulated their Vision and Mission and set BHAGs that energised the whole organisation to strive for and ultimately achieve BHAGs. The goal set by President Kennedy for NASA to put a man on the moon was a BHAG – which typically take several years to achieve.

100,000 MW by 2022 is a BHAG that has stirred the whole Indian industry as well as investors from all over the world, spurring them all into action. In the last ten months or so, after the announcement of the 100,000 MW target, the pipeline of solar projects in India (PPAs signed or RFS issued) has crossed 10,000 MW and is likely to exceed 15,000 MW by end of 2015.

The NTPC has set a target of developing 10,000 MW and purchasing a further 15,000 MW from other developers. It is heartening that SECI has been mandated to develop 20,000 MW of solar park capacity in various states. The Softbank, Bharti and Foxconn joint venture SBG Cleantech plans to develop 20 GW. Sunedison’s target of 15 GW and Rosneft’s plan for 10 GW are all encouraging signs and that Hon’ble Minister for Power, Coal and RE, Shri Piyush Goyal’s statement, ‘I want to kill 10 birds with one stone!’ is indeed turning out to be prophetic.

And that’s not all. There is ‘Make in India’ under which there is strong interest from Indian and foreign manufacturers alike to set up solar-cell manufacturing units. Trina Solar, Sun Edison with Adani, JA Solar, Vikram Solar, Welspun, etc., are some of the manufacturers who are moving their manufacturing plans into top gear.

It is encouraging also to see that the tariffs for solar power, through long-term PPAs of 25 years, are now well under Rs 6.50 per unit and have almost breached the Rs 5 per unit level in the recent tenders in the states of Madhya Pradesh and Telangana. In the tenders in Andhra Pradesh and Rajasthan that are due in the next few weeks, the expected tariffs are in the range of Rs 5 to 5.50 per unit. In a market where the prices of solar cells continue to decline, it is only a matter of time before solar reaches grid parity at Rs 4.50 per unit – especially considering that the interest costs in India at around 12% p.a mean that nearly 60% of the cost of the tariff goes towards servicing the interest on the loan (Share of Cost of Capital in LCOE from IEA’s Solar PV Roadmap 2014). If the interest rates reach single digits, solar will definitely sell for under Rs 5 per unit for 25 years.

Given this tumultuous period for solar, which is both exhilarating and invigorating, I would like to share my views on various policy and regulatory issues, with a view to enabling a renewed and resurgent National Solar Mission to gather steam and reassure and attract investors. My suggestions on the following key areas are given in the table in Annex I.

• Smaller solar parks of 100 to 300 MW

• Completely removing subsidies for grid-connected solar

• Competitive bidding is not a panacea at least for CSP

• Revival of the REC market, India’s alternative to CDM and carbon markets

• Setting of the vision and agenda for R&D in Solar for India to attain a global leadership position

• Distributed generation and solarising the agricultural feeders and

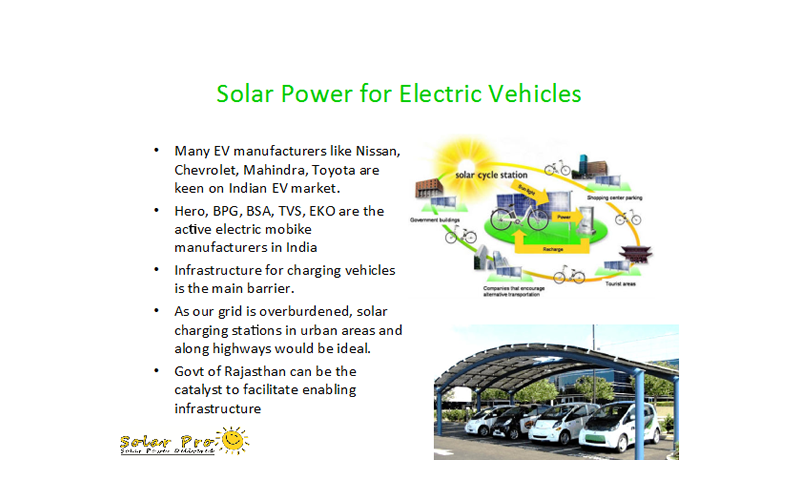

• Solar charging stations for electric vehicles

My vision for solar is not just grid parity but something that can resolve the problems of the power sector. The distributed nature of solar can take generation to the load centres and reduce the T&D losses – the bane of the Indian power sector. This can be the best solution for agricultural pumping in India which consumes over 32% of the total electricity consumption and is mainly responsible for the heavy losses suffered by the distribution companies whose cost to service the farmers is Rs 7 per kWh in many states.

For example, in Rajasthan the connected load of agricultural pumpsets is 9043 MW (about 68% of the total generation capacity is around 15,200 MW) and the agricultural consumption is 15,993 MU, which is 38% of the total energy sales of 42,318 MU. T&D losses are nearly 20%. Solarising the separated agricultural feeders with 1 MW to 3 MW solar plants or going for decentralised off-grid solar pumps with a one-time investment can result in recurring savings of Rs 3780 crores per annum if the T&D losses can be reduced by half to 10%. The total connected load of agricultural pumpsets across the country would be easily over 100,000 MW.

Another emerging opportunity for harnessing solar is for mobility purposes: cars, scooters and bicycles. India imports 80% of its oil and uses over 50% of its foreign exchange for oil imports. The future of mobility is electric vehicles and if EVs were to use solar, this would result in direct savings in terms of oil imports and forex outflow.

A study I carried out in Rajasthan concluded that to displace 5% of the petrol consumed by cars and two-wheelers in Rajasthan would require 21,051 MW of solar power, assuming that only 50% of the charging of the EVs is done through solar and 50% through conventional grid power. Therefore much more than several 100,000 MWs of solar electricity would be required for EVs in future.

Suggestions on Policy and Regulatory Issues - National Solar Mission

|

S. No |

Present Policy / Regulatory Position |

Recommended Future Policy Measures |

|

1 |

Solar Parks: The above-mentioned Scheme for Ultra Mega Solar Projects and Solar Parks of 500 MW is good but excludes solar parks of 100 MW to 500 MW capacity. |

Simple amendment to the Solar Parks Scheme dt 12/12/2014 to include Solar Parks of 100 MW to 500 MW capacity as implementation would be easier because of fewer land aggregation issues. Power evacuation at 132 KV and 220 KV would be simpler and fits the transmission networks at state level. |

|

2 |

Phasing Out Subsidies : Reducing subsidies to 15% from 30% is a great move as they tend to distort the market and lead to inefficient use of resources. |

Please consider:

|

|

3 |

Competitive Bidding: a) The right thing to do and proven to be highly successful for PV projects but resulted in a big disaster for CSP projects. b) The process of competitive bidding is time-consuming and the same may affect achievement of the yearly target additions. c) Success in PV projects was more due to the rapid decline in prices than the bidding process itself. Assessment of the quality of projects is yet to be made. |

a) MNRE should immediately prepare and publish a white paper on CSP projects through an independent international expert and decide the future course of action for CSP projects. b) After price discovery, PPAs may be signed on a ‘first come first served’ basis to save time in the bidding process and to ensure that yearly targets are achieved, in order to meet the ultimate goal of 100 GW by 2022. c) An independent assessment of the projects and benchmarking against quality of projects in Germany or USA will provide good insights for future policy with regard to whether to continue with competitive bidding or adopt preferential tariffs. d) Solar capacity can be added faster than wind by adopting preferential tariffs based on price discovery and regulatory orders. e) Will attract Navratna PSUs and foreign IPPs to invest in a big way. |

|

4 |

REC Scheme: The REC Scheme is simple, straightforward and a great alternative to CDM. But presently enforcement is poor and RECs are not being purchased by state-owned DISCOMs. |

May consider:

|

|

5 |

R&D : The JNNSM document set out various R&D goals but the progress and achievements have not been published. New R&D goals have not been articulated. India continues to lag behind in R&D compared to Germany, USA, Japan and China despite 5 years of JNNSM! |

|

|

6 |

National Clean Energy Fund (NCEF): Doubling the cess on coal was a great idea. Clean energy venture funds were envisaged but are yet to take off. |

|

|

7 |

Entrepreneur Scheme for 1 MW projects totalling 20,000 MW: Lack of clarity in the implementation procedures. Challenges in selection of entrepreneurs in a transparent manner, their capacity development and arranging debt for them. Government is not best suited to handle such a scheme as there would be a high probability of defaults |

The Scheme should be handled by SIDBI or SBI through an Entrepreneurship Development Programme and adopt a selection process used by venture capital/private equity firms. The Scheme should be rolled out carefully in a phased manner, and the entrepreneurs who are successful may be given the opportunity to scale up their projects in the subsequent phases. |

|

8 |

Distributed Generation for Agricultural Feeders No policy at present.

|

We suggest :

|

|

9 |

Solar for Electric Vehicles: Presently no policy in place except for a pilot in Gujarat Secretariat to run minibuses (initiated by Hon’ble PM when he was the then Hon’ble CM).

India imports 80% of its oil and spends 50% of its foreign exchange earnings for oil imports. Solar energy for electric vehicles (EVs) is affordable as there is over 80% saving in fuel costs.

Bhutan has introduced Nissan Leaf to use their cheap hydro power rather than import petroleum products from India. |

According to our study, 5% displacement of petrol used by cars and two-wheelers in Rajasthan will require 20,000 MW if 50% charging comes from solar and 50% from grid. Consider the externalities and multiple benefits of solar charging for EVs. We suggest :

|

DV Satya Kumar is Founder and MD, Shri Shakti Alternative Energy Ltd and can be reached at [email protected]; he blogs occasionally on solar policy and regulatory matters in India at: http://www.ssael.co.in/category/blog/

Download our White Paper